Here’s the opening of an ad from a recent Mark Skousen ad that readers have been asking about:

“PhD Economist Dr. Mark Skousen Makes Stunning Revelation…

“I Made Millions in Pre-IPO Private Placements… And Now I’ve Discovered a Way for You to Do the Same — Without All the Risks.”

“Today I’ll Show You the Fastest (And Most Reliable) Way To Get Rich on Just ONE Investment!”

He’s selling subscriptions to his entry-level newsletter, Forecasts & Strategies ($77 first year, renews at ?), along with a special report called, “The Secret Backdoor into Private Equity Riches” — and he lays it on thick with this “private investments will make you rich” stuff…

“I’ve made millions of dollars in pre-IPO private placements… the kind that are normally reserved for wealthy insiders.

“And today, I’m showing you how you can do the same…

“Without any connections. Without already being rich…

“And without taking all the risks I had to deal with over the years.

“Now, for those of you who don’t know, private equity investing involves getting in on companies BEFORE they go public.

“And it is without question the single, fastest (and most reliable) way to get rich in America today.

“As The Financial Post points out…

‘Of the wealthiest people on the planet, virtually every one of them made their fortune in private equity.'”

And he explains how he has this “secret backdoor” into private equity investing…

“Generally, these sort of opportunities are off limits to regular investors.

“In order to participate in the best private equity deals, you need to either…

“A) Be rich

“Or…

“B) Know somebody important.

“The connections I’ve made over the years have gotten me past the velvet rope, and in on some of the very best deals.

“And these deals have made me very wealthy.

“However, today I want to give you the chance to do the same.

Are you getting our free Daily Update

"reveal" emails? If not,

just click here...“You see… I’ve found perhaps the greatest private equity investment of all time.”

Oooh, oooh, we’re gonna be rich! They’ve been keeping this secret behind a $77 firewall the whole time! Without that, I would be Peter Thiel by now!

OK, maybe not… what else does Skousen say…

“And this time, you DON’T have to be rich to get in.

“You DON’T need to be an accredited investor…

“You DON’T need any special connections… (other than me, of course.)

“And best of all, you DON’T need to take the risks that I had to take to make big money.

“I’ve found a powerful private equity investment that allows you to get in on multiple great private equity deals — all at once.

“And the performance has been out of this world.

“In recent years, for instance, they closed out 7 private equity deals.

“Every single one made money… with the smallest gain coming in at 210%….

“They haven’t exited a single losing position during that time.

“And the amount this private equity investment has paid out to investors has never dropped – not once — in 10 years.”

OK, so some kind of fund? What does he mean by that “paid out to investors” bit? He drops some more clues…

“It’s only grown higher and higher.

“This year it will be $148 million.

“There are no investment minimums. (You can get in for less than $100 if you want.)”

And the big picture argument he makes is not really a “private equity” argument, it’s more of a “venture capital” argument…

“The average company used to go public after 4 or 5 years in business.

“Now the average company goes public after 9 to 10 years.

“As Vox reports, ‘companies are waiting longer and longer to go public.’

“And The New York Times showed this happens ONLY once ‘the company’s fastest phases of growth are behind them.’

“As a result, the public markets are now performing much worse than the private markets….

“The numbers show private equity outperforming the public markets by 50% annually.”

So what else does he tell us about this “secret backdoor” private equity investment and/or venture capital investment?

“It’s the best Private Equity investment I know that you can access from a regular brokerage account… to get into private companies that aren’t available on the U.S. stock exchanges.

“This is a godsend for everyday investors.

“It’s finally a chance to see those big returns you can’t get anywhere outside of Private Equity.

“How’d You Like to Collect 850% In Just Three Years?

“This private equity group made an investment in a new private automotive company just a few years ago.

“The company would have been impossible for regular investors to get into.

“But this private equity group had access.

“So they pooled the money of their regular investors and put in around $2 million.

“Three years later, they sold the position for a $14.4 million profit… representing an 850% gain in just three years.

“Then they distributed the profits to their members.

“And this is not unusual.

“It seems like every single deal they make turns into massive profits for investors.”

So what’s the stock, and what’s the story? Thinkolator sez this is still the stock that Skousen has pitched in the past as his favorite “get rich with private investments” idea, Main Street Capital (MAIN), which is a Business Development Company (BDC) with a pretty good track record from its private financing of smallish businesses. MAIN has been pretty consistent, and has consistently traded at a pretty rich premium to its net asset value (which was $29.54 as of last quarter, so it’s trading at about 1.75X net asset value .. pretty close to where it has often been).

Business Development Companies are pass-through entities, kind of like Real Estate Investment Trusts — they lend to small businesses, usually in part using Small Business Administration funding, and usually also invest in the equity of those companies or get a free equity rider associated with the loan, and they earn a solid return on those loans and investments as long as the customers stay solvent and keep paying on their loans… and since they are a tax-advantaged pass-through, the BDC doesn’t pay corporate taxes as long as they pass along almost all of their income to investors in the form of dividends, so they’re usually pretty high-yield investments.

Main Street Capital, like many BDCs, is a small-to-medium size mezzanine lender — which basically means they lend money to private businesses that need a little more than their local bank can easily supply, but a lot less than it would take to interest Wall Street in a bond issue.

So far this year, MAIN they’re paying 24.5 cents per month, which would annualize out to $2.90, giving MAIN a regular dividend yield of about 5.6%… but they do also pay a special dividend in many quarters, (an extra 30 cents in each of the past two quarters, and 28 cents the two prior quarters), so the actual dividend investors received over the past 12 months (12 monthly dividends plus four bonus quarterly dividends) is $4.07, for a trailing yield of 7.8%.

And that specific investment Skousen references was their investment in Southern RV, which is a small RV dealer in Louisiana and Mississippi that MAIN lent money to back in 2013, and they exited that investment in 2016 — it’s a little bit of an exaggeration to say they had 850% returns, because that was only on the equity “sweetener” in that deal, their returns on the actual first lien loan, which was much larger, were less dramatic. Still, it was certainly a good investment, and it helped MAIN show a profit for its investors. And that’s pretty indicative of the deals that BDCs usually make — they’re not financing startups, they’re providing financing for established small businesses that need capital for growth or business succession or a management buyout, or to deal with an opportunity or a crisis. Think small manufacturers, car dealerships, small restaurant chains, etc., not a bunch of hipsters raising $100 million to start an AI company in Silicon Valley. It’s always possible that one of their portfolio companies gets bought by a larger strategic buyer, but it’s very unlikely that any of them will ever go public.

And to be clear, that particular investment was unusually profitable, and it was eight years ago… and the charts that Mark Skousen shows in the ad are from several years ago, too — here’s the chart he shows of MAIN vs. the S&P 500 and Berkshire Hathaway (BRK-B)… from the look of this chart, which obviously does not include the dramatic market drop that hit everything in March of 2020, it appears that he’s going from the highs of late 2007 to sometime in pre-COVID 2019:

Here’s my version of that chart, as closely as I can match it… I didn’t work that hard to make the performance line up exactly, so he could have picked starting or end points a few weeks differently (or on the starting end, a few months differently) and gotten his ~800% total returns for the stock.

Which doesn’t mean that this particular investment suddenly got awful after 2019 — it has actually continued to do very well, as long as you didn’t sell during the COVID panic — here’s the chart through to today:

Still pretty impressive, right?

But timing does matter, to at least some degree… and I say that only because Mark Skousen’s ads are implying that this is a great investment to make right now, but it’s important to note that MAIN’s strongest performance was in the years from 2007-2017, in part because of multiple expansion as it became a larger and better-known company.

When I go back and look at our archives, it appears that this ad is almost a carbon copy of one he was running in 2019… including that reference to $148 million in payouts “this year” (MAIN should actually pay out closer to $250 million in dividends in 2024… the $148 million number goes back to 2017, so Skousen’s data was very stale even five years ago).

Does that make a difference to the quality of the investment? Not necessarily… MAIN has had very good performance over the long term, and it’s at the upper end of its valuation range but certainly isn’t wildly out of line. The stock might well do just fine going forward, even though we should expect it to be cyclical (meaning, it does worse when the economy goes into recession or slows down, because its small-business customers tend to be somewhat fragile).

But these ads are not ads for an investment, they’re ads to convince you to subscribe to a newsletter, and to that end they’re making a pitch which is obviously lazy and way out of date. Here’s what your performance would have looked like if you bought MAIN the last time we covered Skousen’s pitch, about five years ago — you got a much bigger dowturn from COVID, and a slower recovery, and you’re still lagging the broad market (these are total returns, including dividends, and that’s MAIN in purple):

And that’s probably about what we should have expected — back in 2019, this was my Quick Take for the Irregulars about Main Street Capital:

“This is a BDC that raises equity capital and borrows using debt and SBA funds and lends to middle-market companies, with a little juice from also adding equity investments in smaller companies who need private equity or expansion capital. Good company, very strong track record, monthly dividend that has been growing slowly and is also boosted a bit by two “extra” dividends each year, but trades at a premium price so future returns are likely to be weaker than the past decade’s phenomenal run. I’d also look at the smaller Saratoga Investment (SAR), which is growing fast and is riskier but trades at a lower premium to NAV and with a higher current yield (9% vs. 7%). Haven’t invested in any BDCs in recent years, but it’s a reasonable part of an income investment strategy if you can handle some bumps the next time the economy slows.”

SAR generally kept pace with MAIN after 2019, in case you’re curious, but has lagged this year so the total return is lower now. Haven’t looked at that one since I wrote those words, so I’m not sure why.

And yes, the theme of that 2019 ad was pretty much exactly the same as the one we’re looking at today, the headline was, “I’ll Show You the Fastest (And Most Reliable) Way To Get Rich on Just ONE Investment!” And on that front, the promise of venture capital-like riches falls pretty flat. This is a company that mostly earns 15-20% or so annual returns on its investments when things are going pretty well, pays interest on its own debt and covers their overhead, and passes most of the rest through to shareholders to provide a decent yield — and investors like the yield enough that they’ll pay more than the portfolio is worth, so the real return from current prices is more like 9-10%, and most of that goes out the door to pay the current 8% dividend. That’s the steady state of where we are right now, and where they usually are when things are going pretty well, but it takes only a quick look at the 2020 chart to know that a recession which makes some of their customers stop paying on their loans scares investors (and maybe, for the contrarians, provides a more compelling entry point).

We can take the story back further if you like…

The first ad which we wrote about in which Mark Skousen was teasing Main Street Capital as one of his favorite investments came way back in 2012… to put that in perspective, the pitch of that piece was that MAIN would be a big beneficiary of Mitt Romney winning the presidential election. And it has done, again, pretty well since then… if you reinvested the dividends, your total return would be very impressive. Not as impressive as the stock market in general, but still impressive. This is MAIN (in purple) versus the S&P 500 (orange) starting with that first teaser ad from Skousen, in October of 2012:

Does that bring to mind visions of a 50,000% return on Facebook, and becoming the next Peter Thiel, as the ad kind of implies? No, of course not… this is not a get-rich-quick venture capital investment. It’s private equity (and private credit) investing in small companies that will probably never have explosive growth or be spectacular investments… but a few of the deals will show great returns, and the interest rate is high enough to bring a nice profit, even when they don’t.

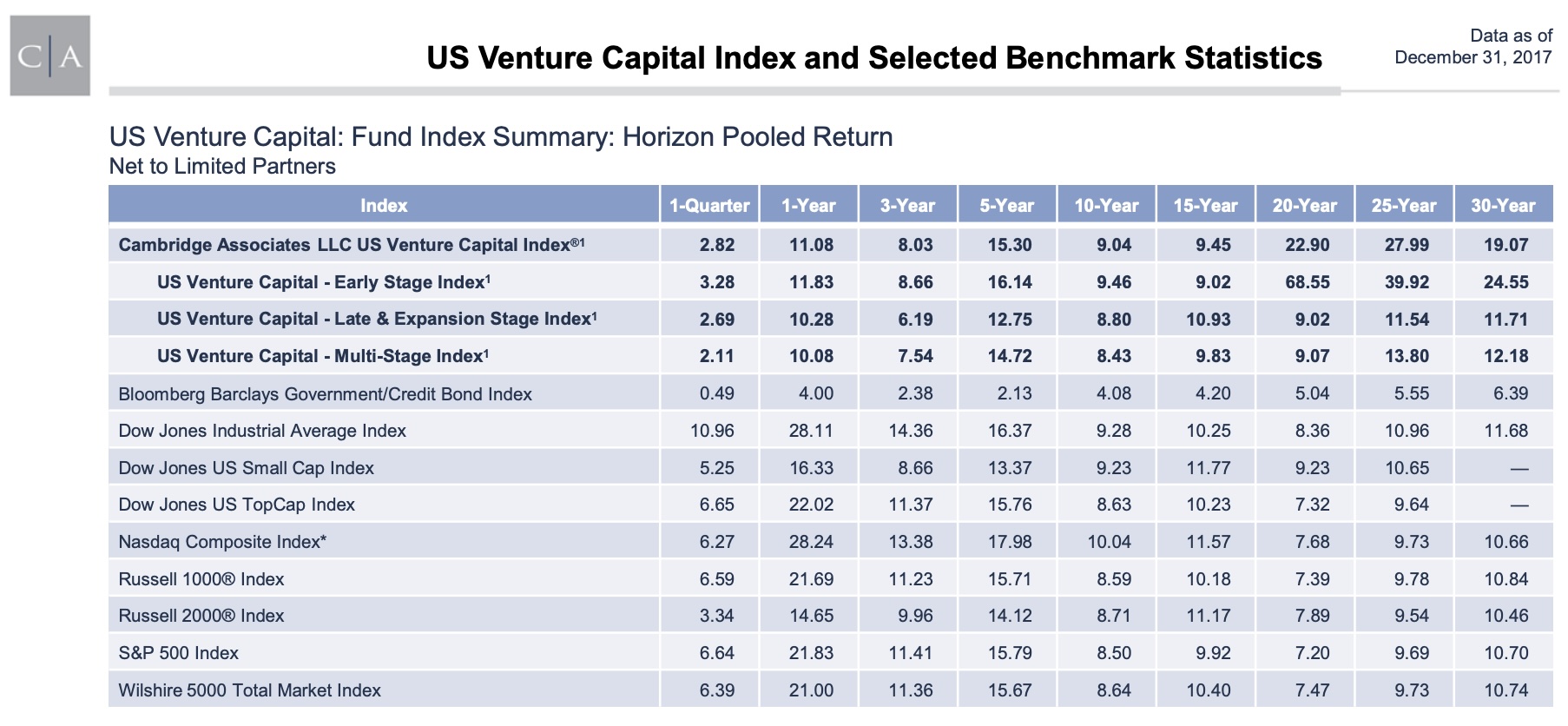

And really, though this isn’t venture capital, I should note that “startup investing” in general is not a “get rich quick” investment strategy, either — there’s a reason why most venture capital funds are committed for ten or twenty years, and that’s because they need a long time to nurture their investee companies, many of which will end up failing, and let the 10% of their investments that really have staying power and go public and grow fast become fantastic winners, to bring up overall returns for their funds. We are conditioned to think of venture capital as being a “home run” kind of business, and to some degree it is, but most of the startup money that doesn’t come from friends and family comes from large private venture capital funds, and the performance of those funds varies a lot — there’s no one standard measure for venture capital performance, and the returns in the 1990s dramatically inflate the longer-term returns, but there have been some historic studies released from time to time. Here’s one from Cambridge Associates presentation in May of 2018, for example:

As of 2017 the net returns from the Cambridge Associates US Venture Capital Index were about the same as the S&P 500 over five, ten and 15 years, but more than double the broad market returns for 20-30 year periods. I suspect we’re probably still seeing average venture capital returns that are similar to broad market returns, because the period when a few funds dominated venture capital in the 1990s is not coming back, and startups have been financed at higher and higher valuations over time (and venture capital funds are people, too, and they’re competitive and get a huge dose of FOMO when their buddies invest in the hot AI startup, so they get way too enthusiastic during big “story” cycles like we’re seeing with AI right now).

But that’s neither here nor there — remember, with BDCs like MAIN we’re financing auto parts manufacturers and staffing firms and coffee house chains, not the next OpenAI.

So I wouldn’t try to talk you out of investing in Main Street Capital or its competitors. They might continue to have good returns, and they pay a solid dividend, though we should be mindful of the impact of higher interest rates and any potential recession in the short term — just remember that no matter what Mark Skousen says, you’re not going to get “I bought Facebook when Mark Zuckberberg was still at Harvard” kind of returns. Not even close.

If you want to try to get extreme returns, get into angel investing and pick specific companies you want to back, whether that’s your friend’s restaurant or a local entrepreneur or an idea from one of the many online startup marketplaces — but be mindful that the odds are very high that you will never be able to pull your money back out, and the odds are low that it will turn into a dramatically successful investment with a profitable “exit.”

Really, what Main Street Capital is doing is much more akin to what we think of as “private equity” and “private credit” these days — and they’re doing it with the smaller companies that don’t attract the attention of KKR or Blackstone or Brookfield or the other big private equity managers. And they’re pretty good at it, with steady dividends that provide some solidly compounding returns — but so far, unless you happened across MAIN when they were small and cheap and everyone was afraid of private equity in their first couple years, during the 2007-2009 financial crisis, investing in MAIN provided about the same returns as investing in the S&P 500, usually a little less.

Maybe that will be different going forward, but I’d guess that over the next few years MAIN will probably provide meaningful outperformance only if there’s a meaningful decline in interest rates, which would make investors accept a lower yield for owning MAIN shares and therefore help boost the price… though that would boost many other dividend-focused companies as well, from REITs to MLPs to other high-dividend financial companies.

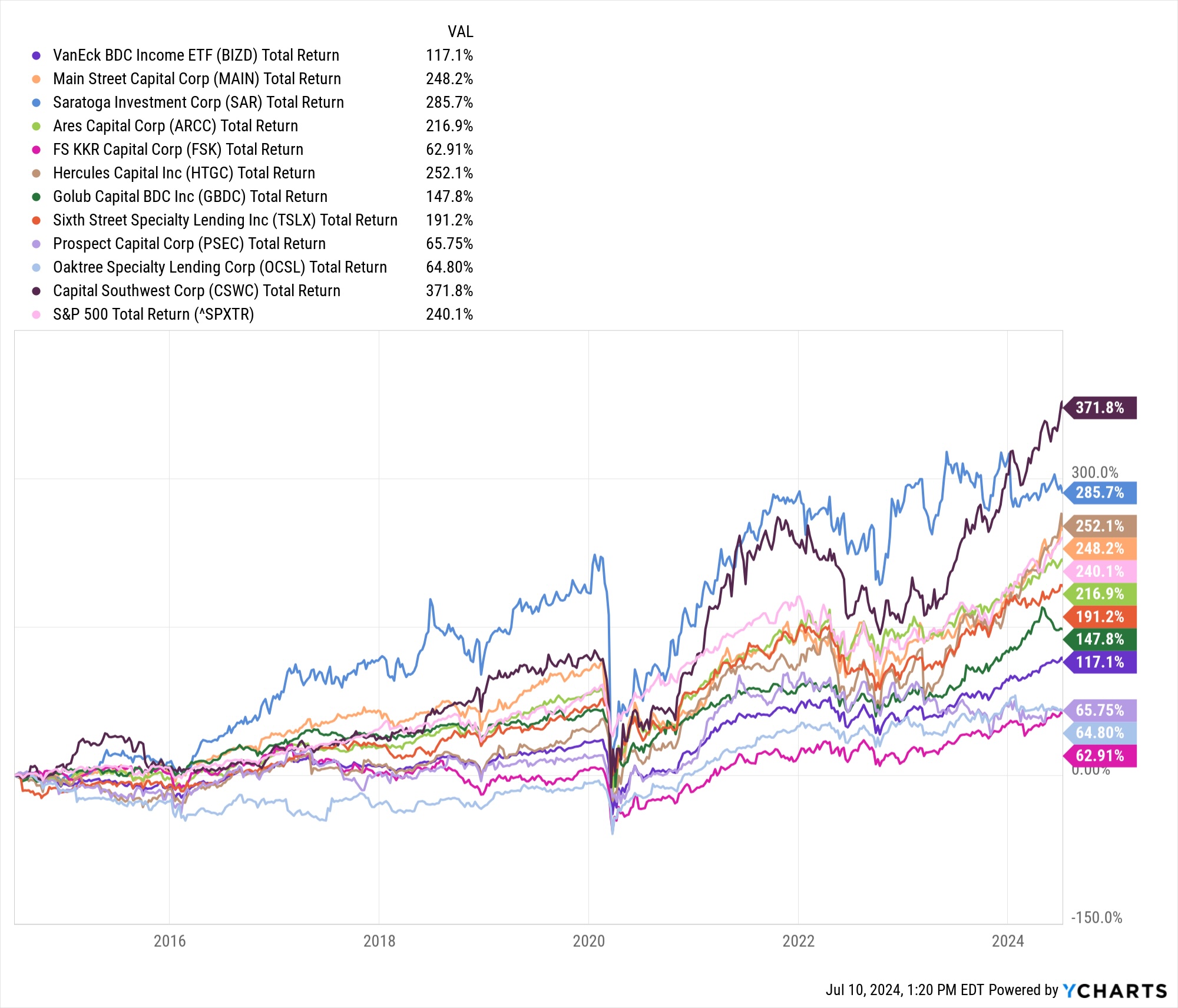

Here’s the total return chart for the past ten years of all the BDCs I can think of that have been around that long, just FYI — and of the Van Eck BDC Income ETF (BIZD), which holds most of these names — so you can see that a handful have roughly matched or done a little better than the S&P 500 during that time, and about 2/3 have significantly underperformed the broad market… but the average, as represented by the BIZD ETF in purple, is pretty terrible (MAIN is in orange, roughly matching the S&P 500 for this time period, in pink):

I’m actually a little bit surprised that the BDCs have done as well as they have over the past year, given the rise in interest rates, but here’s that one-year chart — again, several of them (including MAIN, as well as HTGC, which also gets teased pretty regularly) have matched or beaten the S&P 500 over the past 12 months, despite not owning any of the “hot” stocks, and the ETF has almost kept up with the S&P.

Maybe that’s just anticipation of this solid economic environment continuing, maybe it’s just yield-seeking now that folks are less worried about interest rates going up further, but it’s a little surprising. And encouraging.

Here’s the chart of some broader high-yield asset classes over the past decade, which again makes the total return of BDCs look somewhat reasonable — that’s the BDC ETF in purple, trailing only the high dividend yield ETF (VYM, which owns plenty of hot stocks like Broadcom and comes much closer than any of the others to keeping up with the S&P 500’s wild bull run over the past decade — that’s the S&P 500 in brown), so BDCs have held up a lot better through the decade that brought us the Euro crisis, the COVID panic, and both the collapse to zero rates and the rise of inflation and interest rates, than have most REITs (orange), junk bonds (pink), or MLPs blue). Which is saying something.

And I was curious about which of these income-focused assets are most volatile, and therefore most interesting when things get ugly — so I checked to see what it would be like if we bought all those in the heat of the COVID panic, in late March of 2020.

Turns out, like MLPs, the BDCs were generally a great buy during the worst part of the COVID panic, because they got clobbered much harder than the others during that month — so that’s worth remembering, next time we see a market collapse. Maybe these are the kinds of investments that are more prone to overreaction, because investors see them as somewhat more fragile… so we might want to consider them at times when there’s real panic in the markets, not get excited about them when everything is “mostly OK.”

That’s just my two cents, though, and I don’t own any BDCs (I do have a big allocation to the Alerian MLP ETF)… when it comes to your money, you get to make the call — do you see something to like in this small business lender? Have other income investments you like… or, perhaps, even some “make you a millionaire fast” investments you think we should consider? Let us know with a comment below. Thanks for reading!

Disclosure: Of the investments mentioned above, I own shares of the Alerian MLP ETF. I will not trade in any covered investment for at least three days after publication, per Stock Gumshoe’s trading rules.

Well besides BIZD, if you want a one stop solution for the BDC environment there is also PBDC (by Putnam) that pays a decent yield and has most of the big players in their top 10.

Yep, PBDC is newer so I didn’t use it for the comparisons (has only been around since late last year) — but for what it’s worth, it has outperformed BIZD during its young life, looks like that’s largely because it has less allocated to the largest BDC, Ares Capital (ARCC), which has lagged the index a little, and has a bigger allocation to Blue Owl (OWL), which has had a great year.

Is this the best we can get from a PhD Economist?

Not many PhD’s write their dissertation on stock picking, I imagine.

I am a bit confused is comparing a single stock to an index like s&P500 meaningful or fair in general?

I think we should generally compare any single stock to either the S&P 500 or, in some cases, to some other relevant index — the S&P 500 is the most widely accepted proxy for the average performance of the stock market, so if you’re judging the performance of an individual stock then comparing it to the average is the fairest way to look at it, and to judge whether the stock was average, below average, or above average.

That doesn’t mean stocks with below-average performance were necessarily bad picks — that depends on what you’re looking for as an investor. Lots of investors need income and are willing to accept a lower return in order to receive income, or want to diversify among different types of companies even though we know that some of those stocks will go through many years of below-average performance (we just don’t know which ones).

I use the S&P 500 as the benchmark for all teaser picks — essentially because all teased stocks are promoted as being dramatically above average, but we also know that we can buy the S&P 500 index and get average performance for almost no cost, and without doing any work. It has never been easier or cheaper to guarantee yourself average performance, so we should be aware of the risk we take in trying to do better than average. In some cases it would be better to use a global average, or the small cap average, or something else, but I consistently use the S&P 500 for consistency.

I have met Mark Skousen at the Money Show and he is one of the best presenters they have. I bought MAIN in 2020 and my gain after cost basis of 100 k in 2 buys is 150 K. Not many stocks do that well. It may not be NVDA but my profit is excellent.

Yes, I think I shared a chart above about the performance of these more volatile income instruments during the COVID downturn — MAIN and the rest of the BDCs were more beaten down than the broad market in 2020, and bounced back more dramatically as well (though it took longer — the market was hitting new highs again by August of 2020, the BDCs didn’t get back to their 2019 highs until the Spring of 2021).

I’ve had a chunk of MAIN since 2019 and bought it on a dip when others were freaking out. I doubled my position at one point along the line at another freakout point. I have always reinvested the dividends over all this time, too, bringing the overall yield to 128% which is 20% per year. MAIN has been a successful investment! The way to invest in BDC’s it to identify which ones are quality, buy on a dip and hold on!

I currently own a dozen quality BDC’s to (diversify amongst BDC’s) and the overall portfolio is yielding 21% per year for almost 5 years now.

Forecasts and Strategies is a decent newsletter. Much of it is advertisements for Shousen’s other services and the many books he has written but there is some good advice. I’ve met him several times and think he’s a smart guy.

MAIN is the correct answer. I bought it many years ago based on his recommendation. I still own it and have collected many dollars in dividends and have a large unrealized capital gain. I like that the dividends are monthly.